After buying homes for cash since 2020, I can tell you the call I dread most isn’t from a seller who has a tough property or a complicated situation.

It’s from a seller who went with another buyer’s offer — one that came in higher than mine — and is now three weeks from their moving date with no closed deal and no clear answers.

It happens more than you’d think.

When homeowners start shopping cash buyers, the question is almost always the same: who’s going to give me the most money? That’s a completely reasonable place to start. You’re selling a major asset — of course price matters.

But after hundreds of transactions, here’s what I’ve learned: the highest offer and the best offer are often two very different things — and the gap between them is where sellers get hurt.

Delayed closings. Last-minute renegotiations. Fees that appear out of nowhere at the closing table. Deals that fall apart entirely two days before you were supposed to move.

These aren’t rare edge cases. They’re what happens when the offer number is the only thing that gets evaluated.

The Problem With “Too Good to Be True” Offers

Some buyers know that the fastest way to win a deal is simple: offer more than everyone else.

At first glance, that sounds great. You get multiple offers, one comes in noticeably higher than the rest, and it feels like an obvious choice.

But here’s what I’ve watched happen over and over: that high number is often just the opening move in a negotiation strategy. It’s designed to get you under contract — not to reflect what the buyer actually intends to pay.

Once you’re locked in, the leverage shifts. And that’s when the price starts to move.

This tactic has a name in the industry: re-trading.

What Re-Trading Actually Looks Like

Re-trading is when a buyer makes an attractive offer, waits for you to get emotionally and logistically committed to the deal, and then finds a reason to lower the price before closing.

I’ve seen it triggered by inspections, final walkthroughs, title review, and what buyers call “financing checks” — even when the deal was supposedly all cash. The specific trigger almost doesn’t matter. What matters is the timing: it always comes late, after you’ve already mentally moved on.

The script usually sounds something like this:

“We found more issues than we expected.” “Our numbers shifted — we need to come down a bit.” “The market changed since we made the offer.”

And just like that, the number drops. Sometimes $5,000. Sometimes $20,000 or more.

By that point, most sellers are stuck. They’ve packed. They’ve made plans. They’ve already told their family they’re moving. Starting over means re-listing, new negotiations, more carrying costs, and blowing up whatever comes next. So they take the lower number just to be done with it.

That’s not a coincidence. It’s the strategy.

Why This Works So Well on Sellers

I want to be honest about something: re-trading works because it targets sellers at their most vulnerable moment.

The sellers I’ve spoken to who went through this weren’t careless or naive. They were dealing with real pressure — an inherited home they couldn’t afford to carry, a relocation deadline, a divorce that needed to be finalized. They made a reasonable decision based on the information they had.

The problem is that a high offer number, on its own, tells you almost nothing about whether the deal will actually close at that number.

What it does tell you is that the buyer knows how to make an offer look attractive. That’s a sales skill, not a reliability signal.

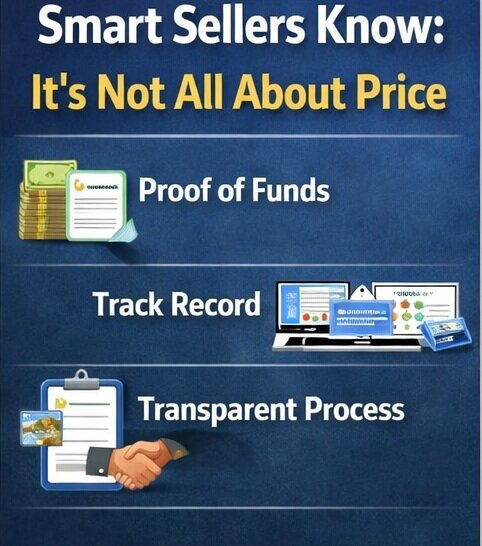

What to Evaluate Instead

When I talk to sellers who are comparing offers, I tell them to think about four things beyond the number:

1. Proof of funds

Any legitimate cash buyer should be able to show you — immediately, without hesitation — that the money actually exists. A bank statement, a proof of funds letter, something verifiable. If a buyer deflects or delays on this, that’s your answer.

When sellers ask me for proof of funds, I send it the same day. It’s a basic ask and there’s no reason not to.

2. A track record you can actually verify

Look them up. Not just their website — their reviews. Google, Facebook, the BBB. Look for patterns: do they close on time? Do sellers say the final number matched the offer? Are there complaints about last-minute price changes?

A buyer who’s completed hundreds of legitimate transactions has a paper trail. If you can’t find one, be cautious.

3. Transparency about the process

A trustworthy buyer should be able to walk you through exactly what happens between contract and closing — without vague answers or evasion. How do they determine their offer? Are there any fees deducted at closing? Under what circumstances might the offer change?

If the answer to that last question is “it won’t” and they can back that up with their track record, that matters.

4. An offer that was realistic from the start

Buyers who lowball on the first call and negotiate up are easy to spot. But re-traders go the other direction — they come in high and negotiate down. A buyer who makes a serious, well-reasoned offer based on actual comps and condition is less likely to come back to you later with a revised number. The offer reflects real math, not a strategy.

The Question You Should Actually Be Asking

Most sellers go into this process asking: what’s the highest offer I can get?

After seeing how this plays out hundreds of times, I’d encourage you to ask a different question: which buyer is actually going to close at the number they’re offering?

A deal that closes on time, at the agreed price, with no surprises is worth more than a higher number that evaporates three weeks before closing. The carrying costs alone — mortgage, taxes, insurance, utilities — can run $2,000–$3,000 a month on a vacant or transitional property. Every month a deal falls apart and you start over is real money out of your pocket.

Certainty has real dollar value. Don’t give it away chasing a number that was never real.

How to Protect Yourself Before You Sign Anything

Before you accept any cash offer, here’s what I’d recommend:

- Ask for proof of funds in writing — and verify it’s current, not months old

- Request the full offer in writing with clear terms before you agree to anything verbally

- Search for reviews independently — don’t rely on testimonials on the buyer’s own website

- Ask directly: will this offer change after inspection? — a confident, legitimate buyer will answer this clearly

- Ask about fees — some buyers advertise “no fees” but deduct costs at closing under different names; get it in writing

A buyer who has nothing to hide will welcome these questions. If asking for proof of funds or a straight answer about fees makes a buyer uncomfortable, that discomfort is telling you something important.

The Bottom Line

Get multiple offers. Compare them. That’s always the right move.

But when you’re comparing, don’t stop at the number. Look at who’s behind it — their track record, their transparency, their willingness to show you the math and answer hard questions without flinching.

The best cash offer isn’t always the highest one. It’s the one that actually closes.

Want to Know What We’d Offer?

At 3 Step Home Sale, we’ve been buying homes since 2020. Our offers are based on real numbers — local comps, actual condition, honest math. We’ll show you exactly how we got there, answer every question you have, and if it makes sense for both sides, we’ll close on your timeline.

No pressure. No surprises. No last-minute renegotiations.

Get your free cash offer at 3stephomesale.com →

Frequently Asked Questions

Why do some cash buyers offer more than others? Some buyers deliberately come in high to win the contract, then renegotiate the price later during inspections or before closing — a practice called re-trading. A high offer is only meaningful if the buyer has a track record of actually closing at that number.

Should I just accept the highest cash offer? Not automatically. A slightly lower offer from a buyer with verified funds, strong reviews, and a transparent process is often the safer choice. The offer that closes on time at the agreed price is the best offer — regardless of which number looked biggest on paper.

How do I know if a cash buyer is legitimate? Ask for proof of funds, look up independent reviews, and ask directly whether the offer could change after inspection. Legitimate buyers answer these questions without hesitation. Evasion or deflection is a red flag.

Can a cash buyer lower their offer after I accept it? Some will try. The best protection is asking upfront — before you sign — whether the offer is subject to change, and working with buyers who have a documented history of closing at the offered price.